When people talk about financial mistakes, they often think of scams, bad investments, or losing money in the stock market. But my biggest mistake didn’t come from a bad tip or trusting the wrong person. It came from something much simpler — not knowing how to manage my finances.

At that point in my life, I was just a university student at MIT. I was good at earning income — I worked part-time and received a scholarship from Yayasan Tenaga Nasional (YTN). But I had no clue how to manage my money.

I believed in delayed gratification. Back home in Malaysia, I had grown up with the understanding that if you wanted something, you worked hard, saved up, and bought it when you could afford it. Credit wasn’t even part of the equation.

But that changed when I went to the U.S.

My First Taste of Debt

I opened a checking account with Fleet Bank and was given a USD 300 overdraft facility. At first, it felt like a safety net — not something I’d need, just something that was there. For the first two years, I didn’t even touch it. Between my scholarship and my income from working at the MIT Sloan Computer Lab (and later the MIT Summer Professional Office), I was doing okay.

But things began to change. I was juggling more responsibilities — helping a friend who had been suspended from university, and also starting a relationship with someone special (who’s now my wife — but that’s a story for another day).

Spring Break and the Road Trip That Cost Me

Spring break in my freshman year, I went on a road trip to Miami with two friends from out of town. We couldn’t rent a car ourselves (none of us were 21 yet), so I asked a senior from MIT, Iqbal, to book it for us. He agreed — but didn’t join the trip.

The journey from Boston to Miami was an adventure. We rotated roles — driver, navigator, and sleeper — using printed maps from Yahoo (no GPS back then!). But everything changed in South Carolina. We switched drivers around 6–7 a.m. I moved from the driver’s seat to be the navigator. The new driver, who had the least experience and refused to freshen up, took the wheel.

Minutes later, we were in the middle of the road, confused about which exit to take. Out of nowhere, a car slammed into us. Ours spun several times. I still remember the fried chicken and chili sauce flying through the air — our friend in the back wasn’t wearing his seatbelt.

We weren’t injured, but the car was totaled.

Since the person who rented the car wasn’t with us, the rental company held us fully liable. We agreed to split the damages — USD 5,000 each, to be paid over 10 quarters. That was a huge financial burden. But we still rented another car, finished the trip, and returned to Boston — now carrying a long-term debt as university students.

The Slippery Slope of Credit

Despite the new financial burden, I still didn’t touch my overdraft. I didn’t even use the credit cards that banks kept sending me. But in my junior year, I made another decision that would accelerate my downfall: I stopped working part-time so I could focus on taking the maximum credit hours allowed.

Without part-time income, I still continued spending as if nothing had changed. I bought PS2 games, went to movies, ate out, and traveled to Michigan to visit my girlfriend. I justified it by telling myself:

“I’ll get my scholarship soon.”

“I’ve already secured another part-time job after summer.”

But the credit card balances kept growing. The interest started piling on.

By the end of summer of my junior year, I had maxed out multiple credit cards, owing USD 10,000 (about RM 38,000). That was a huge amount for someone with no fixed income and no savings.

Rock Bottom

I still remember one particular trip to Michigan. I had no savings. My credit cards were maxed out. But I still flew out — believing that my YTN allowance would be in soon. My girlfriend and I lived off her pantry: rice, eggs, soy sauce, and crushed Pringles for variety.

Then the worst happened — a delay in the scholarship disbursement. Suddenly, I had nothing left to fall back on.

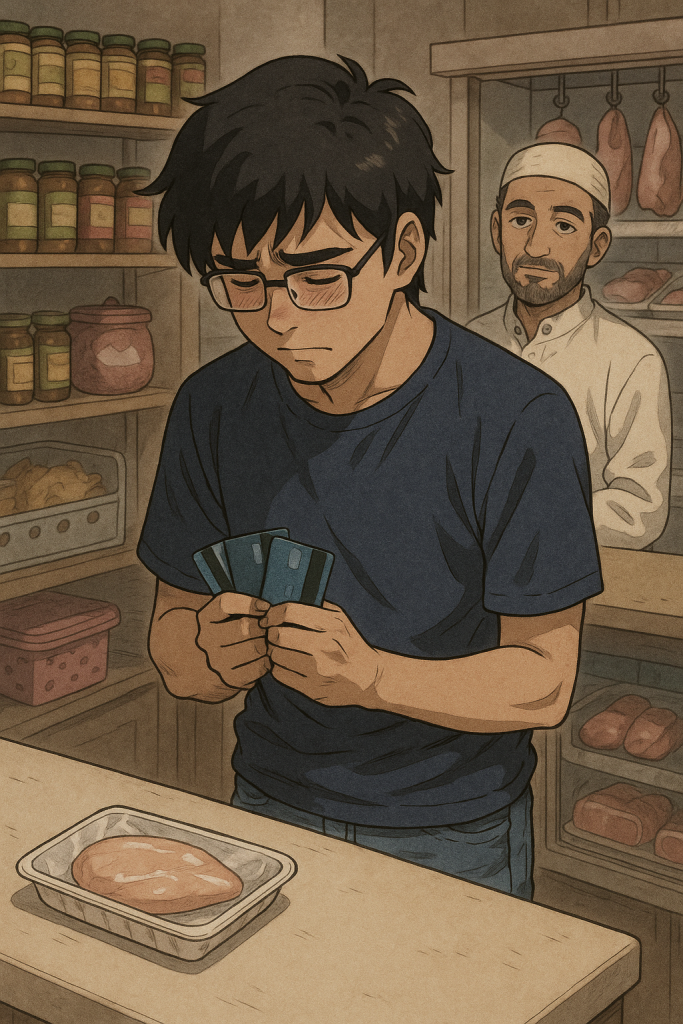

One day, we took the bus to a halal butcher to buy a piece of chicken breast. It cost about USD 3. I had to split the cost between three credit cards — swiping 80 cents on one, USD 1.20 on another, and hoping the third one would go through.

The cashier, a Middle Eastern man, said something that stuck with me forever:

“Brother, even if the last card didn’t work, I would have still let you take the chicken.”

I nodded in gratitude, but inside, I was crushed.

How did I — someone resourceful, driven, smart — end up in this position?

Lessons I Carry for Life

That moment was my wake-up call.

It wasn’t just about being broke.

It was about realizing I had lost control of my financial decisions.

It’s also the reason why today, as a licensed financial planner, I never judge anyone for their debt problems. I’ve lived it. I’ve been that student who looked confident on the outside, but was struggling behind the scenes.

This chapter of my life taught me:

- Debt doesn’t start with irresponsibility — it starts with unawareness

- Pride can blind you from asking for help

- Financial resilience isn’t about how much you earn, but how well you manage what you have

In the next chapter, I’ll share how I started crawling out of this hole — slowly, intentionally, one decision at a time.

Because making mistakes is human. But learning from them? That’s what changes lives.

One Response