In 2013, researchers Sendhil Mullainathan and Eldar Shafir conducted a study to explore how financial stress impacts our cognitive abilities.

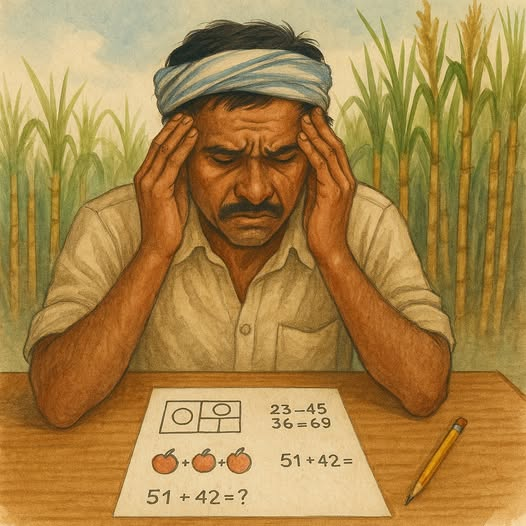

They worked with 464 sugarcane farmers in Tamil Nadu, India—individuals who typically receive most of their income after the annual harvest. Each farmer took cognitive tests twice: once before the harvest (a financially tight period) and once after (when their finances were more stable).

The results were striking. The farmers performed significantly worse on the tests before the harvest. The drop in cognitive function was equivalent to losing 13 IQ points—similar to the effect of pulling an all-nighter.

This is the psychology of scarcity at work. When money is tight, our minds are consumed by the pressure of making ends meet. Our decision-making suffers—not because we’re incapable, but because we’re overwhelmed.

As a financial planner, I’ve seen this firsthand.

People in financial distress often make decisions that worsen their situations, not due to a lack of knowledge, but because they simply don’t have better options. I’ve worked with business owners who sell at a loss just to keep the cash flowing, or individuals who rack up credit card debt to handle unexpected expenses. Some remain in toxic jobs because their finances give them no other choice.

But here’s the good news: once these same individuals achieve financial stability, their decisions improve, and their lives follow suit.

With support and structure, a struggling client can begin making confident, long-term decisions. One client stopped chasing small salary bumps and focused on building his skills. The result? A 100% salary increase over four years.

Another client moved away from low-margin work that drained their team and finances. With stability, they were able to pursue higher-quality clients and watched profits grow.

The ability to make better choices is in all of us. The question is: when will you give yourself the financial space to make them?